DVS Weekly Update 2026-10 (Part II): Respect Risk, Reposition Capital

In Part I we zoomed out and looked at the bigger map rather than one single company. The key message was straightforward: precious metals had reached a point where the long-term rails were saying “cool off and respect risk”, while parts of energy, uranium and critical metals were still earlier in their move.

That was the logic behind the larger-than-usual Core 15 reshuffle. A few names left not because they were suddenly broken, but because better risk-reward had opened up elsewhere. Capital was being recycled away from stretched or slower setups and into areas where the structure still looked cleaner, earlier and more asymmetric over the next 12–24 months.

That matters here, because natural gas fits that broader framework quite well.

Gas is no longer in panic mode, but it is also far from irrelevant. The easy “nobody cares” phase is gone. What we have instead is a market that still sits in an awkward middle ground: less euphoric than oil at times, less loved than uranium, but still system-critical and still capable of repricing violently when supply, weather or geopolitics wobble.

That is what keeps me interested. Strip away the noise and gas still checks a few important boxes: energy security, grid flexibility, and periodic upside torque when the market gets too complacent. I do not need it to become the hottest commodity on the planet; I just need it to remain important enough that the right small-cap equities can rerate when the tape tightens.

That is also why I prefer to express the theme through selected equities rather than trying to dance in and out of the front-month contract every time headlines flare up. I want existing production, infrastructure already in place, some visible path to incremental volumes, and jurisdictions where domestic gas is treated as useful rather than politically toxic. In other words: small companies with real assets, real leverage and at least some operational self-help.

If you follow me on X, you already know I have been vocal on Southern Energy (SOU.v) as one way to play the North American side of that setup. The company below gives me a different angle: a tiny European-listed gas and gas-to-power story with multiple producing assets, existing infrastructure and several paths to grow into its current valuation.

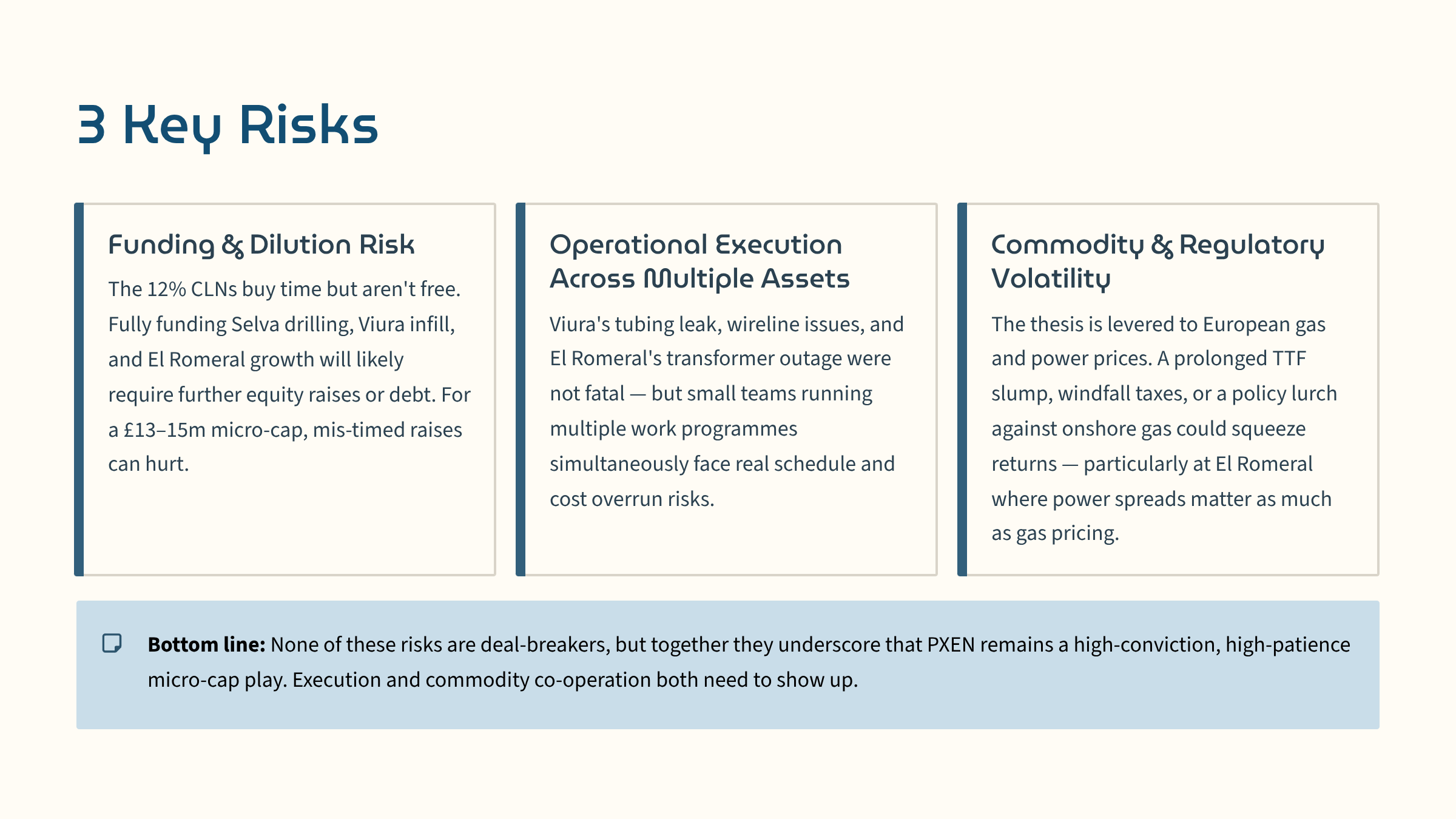

It is not a Core 15 anchor, and I do not treat it like one. This is classic micro-cap natural gas idea territory: small size, real cash flow, genuine upside if gas behaves, but also the usual mix of funding, execution and local regulatory risk that comes with the territory.

That combination is exactly why it is interesting. If the macro holds together, you get meaningful torque off a very small market cap. If it does not, this is still the kind of position that belongs in a smaller sleeve of the book rather than at the centre of it.

At the same time, if you are still heavily long precious metals here - whether that is platinum via something like PPLT, gold via GLD, silver via SLV, or miners more broadly - I do not think it is a bad idea to at least consider some longer-dated put options as insurance on part of that exposure. Not because I am calling for the end of the world or saying platinum is heading back to 1,000 tomorrow, but because structurally a few of these charts are starting to look a bit sloppy on the daily, and if you followed my weekend notes, you will know why I have been leaning more cautious here.

Think of it less as a bearish bet and more as portfolio insurance. Just like you insure your car or your health, you can insure a mining- or metals-heavy portfolio too. One way some investors do that is by looking at puts 12 to 18 months out, sometimes even 24 months, either around the money or roughly 5–10% out of the money, depending on how much protection they want versus how much premium they are willing to pay.

Very simply, a put option gives you the right to sell an asset at a set price before a certain date. So if the underlying drops hard, that put can rise in value and help offset some of the pain in your longs. If metals do break higher instead, you have not “blown up” your portfolio; you have just paid a premium for insurance, and in many cases you can still sell those puts back later, potentially at only a modest loss depending on timing and volatility.

Again, this is not me saying everyone must hedge here. It depends on your sizing, time horizon, conviction and whether you are leveraged or not. But if you are very exposed to precious metals after a big move, I do think it is worth at least thinking about risk management here rather than only upside.

And for anyone newer to options: calls are generally used when you want upside exposure; puts are generally used either to speculate on downside or to hedge an existing long position.

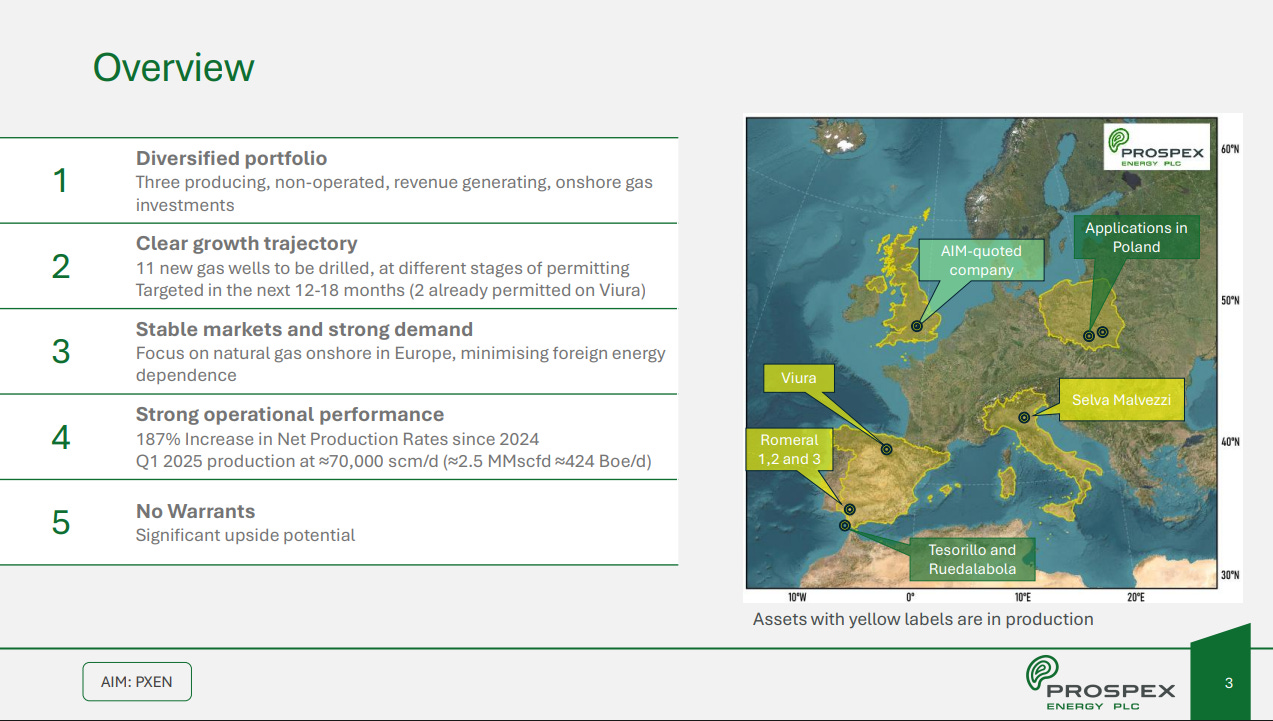

Micro-Cap Natural Gas Idea | Prospex Energy (PXEN.L)

Asset Overview | Selva (Italy) + Viura & El Romeral (Spain)

Prospex Energy is a tiny AIM-listed European gas and gas-to-power company built around three producing onshore assets in Italy and Spain, plus one longer-dated exploration permit. The core portfolio consists of the Selva Malvezzi gas concession in northern Italy, the Viura gas field in northern Spain, and the El Romeral gas-to-power complex in southern Spain.

Selva is the clearest cash-flow anchor today. Prospex holds a 37% working interest, and the PM-1 well has now been onstream long enough to prove that this is not just a paper reserve story. 2025 gross production topped 1 Bcf, with independently verified 2P reserves of 13.4 Bcf gross, plus meaningful 2C and prospective upside nearby. The real attraction here is not just the current well, but the ability to use the existing infrastructure as a base for further near-field development.

Viura adds scale and growth. Prospex’s effective economic interest is only 7.24%, but the structure is attractive: until its capital commitment and preferred return are repaid, it receives 14.47% of production income. Remaining 2P reserves are estimated at roughly 90 Bcf gross, and after operational issues during 2025 the Viura-1B well was brought back online in October and is ramping again toward plateau production. In other words, this is a producing Spanish gas field with real reserve depth and a temporarily enhanced payback structure.

El Romeral gives the story a slightly different angle. Prospex owns 49.9% of a cluster of small gas fields feeding an 8.1 MW gas-fired power plant in Andalucía. The project recently secured a 10-year licence extension to 2034, and after a frustrating transformer-related shutdown through the second half of 2025, electricity generation resumed in January 2026. There is also upside from additional wells and a potential solar expansion, which could gradually turn it into a broader gas-plus-power platform rather than a simple legacy asset.

The final piece is Tesorillo in southern Spain, where Prospex holds 15% with an option to move higher. It is a large speculative gas concept that has been stuck in permitting limbo for years, so I would treat it as optionality rather than something central to the near-term case.

That is really the appeal here: one Italian gas field, two Spanish gas/gas-to-power assets, existing infrastructure, real production and multiple self-help levers, all wrapped inside a very small market cap.

Development Focus & Operational Progress

Over the last few quarters the company has shifted from “prove the concept” into a more practical phase: operate better, stabilise production, and line up the next steps.

At Selva, the main progress has been the completion of a 3D seismic survey, continued stable production from PM-1, and the confirmation of a reserve and resource base that supports more than just a one-well story. The goal now is straightforward: identify the best near-field targets and gradually convert more contingent and prospective gas into booked reserves.

At Viura, the main story has been recovery. The field hit operational issues in 2025, but the restart of Viura-1B in October and the subsequent move back toward stable production matter because this is the asset with the biggest reserve base and one of the clearest routes to higher cash flow. Further wells are planned for 2026, so the field still has genuine growth potential rather than simply decline management.

At El Romeral, the key change is that the outage is largely behind the company. Generation is back, the licence extension is in place, and the custom transformer due later this year should remove the temporary nature of the current setup. It is still the messiest of the three assets operationally, but also one of the more interesting if management can execute on the next development phase.

There has also been a leadership change, with Tom Reynolds taking over as CEO in February 2026. Given his background in small listed E&Ps and corporate transactions, the read-through is fairly clear: sharpen the portfolio, improve capital allocation, and try to turn a collection of small assets into a more coherent value story.

Financial Position & Strategic Angle

PXEN is very much a micro-cap. At recent prices, the company sits around a ~£15m market cap, which is small relative to the fact it already has three producing assets and a material reserve base. That small size is part of the attraction, but obviously also part of the risk.

The balance sheet is not fortress-like. Prospex has funded a good portion of recent development from internal cash flow, but it has also relied on equity and, more recently, a £1.6m convertible loan note. That removes some immediate pressure, but it also reminds you this is still a growing small-cap, not a self-funding major with unlimited room for error.

Strategically, though, the company is quite well positioned. All three producing assets sit in places where domestic gas still has political relevance. Italy and Spain are not perfect jurisdictions, but they are stable, infrastructure-rich and increasingly aware of the value of home-grown energy supply. In a Europe that remains structurally more dependent on LNG and more exposed to geopolitical shocks than it was pre-2021, small onshore gas projects with existing pipes and plants can carry more strategic value than the market sometimes gives them credit for.

That is why I find PXEN interesting. You are effectively buying a geared micro-cap natural gas idea with real production, real infrastructure and several tangible self-help levers. It is not the kind of name I would build a portfolio around, but it is exactly the kind of small-cap gas story that can work well if the macro backdrop stays supportive and management executes even reasonably well.

From here, we transition into the two new energy picks that I pushed straight into the Core 15 as part of an even bigger tilt toward energy.

For those newer here, it’s probably worth revisiting the Energy Special (here) I published in early February, because that note lays out the broader framework for why I’ve been leaning more aggressively into the space.