Hecla Mining: Bellwether, Not Bargain

Over the next few months I’m rolling out something new for both free and paid subscribers: a bi-weekly deep dive into a single company within the broader commodities universe.

The idea is simple:

Sometimes it’ll be a stock I don’t own (yet).

Sometimes it’ll come straight from my larger personal watchlist; which is far broader than the Core 15.

Sometimes it’ll be something I’ve mentioned on X but never actually unpacked.

And sometimes it’ll be a bigger, more liquid name that sits well outside my usual asymmetric microcap hunting ground.

The point is not to hand out buy signals.

The point is simple: to give you a proper framework, what the business actually is, where the numbers sit today, what the market is pricing in, and how I personally treat it inside the rotation map. The full Core 15, niche lists and real-time rotation work remain for paid subscribers, but these deep dives themselves will stay open so everyone can follow along.

If you enjoy this level of detail, just know that work like this is only possible thanks to the support of paid subscribers. I don’t run a Patreon or donations page; Substack is the only place to do that. If you want to support the work, unlock the full map, or simply get more access, you can upgrade any time. I’m also running a Black Friday special until 29 November 2025: 33.3% off annual subscriptions. Zero pressure but it genuinely makes a difference.

Why start the series with Hecla Mining?

Because I want to begin with a name that sits well above my usual universe.

Hecla Mining (NYSE: HL) is not obscure.

It’s not a “hidden gem.”

And it’s not a junior searching for its first orebody.

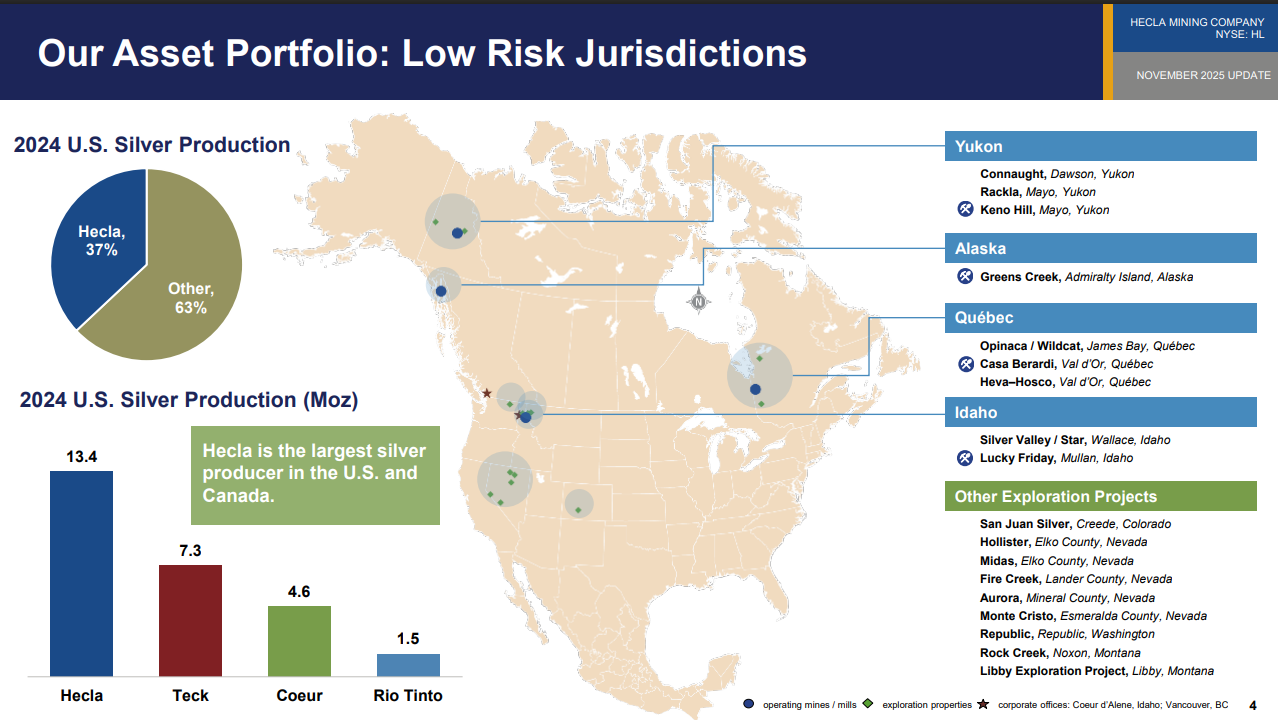

It’s the largest primary silver producer in the United States and Canada, with the company’s own materials putting its share at roughly 37% of U.S. silver production and about 29% of Canadian silver production. It operates only in tier-1 jurisdictions - Alaska, Idaho, Quebec, the Yukon - and has been around for more than 130 years.

2024 was already a major year:

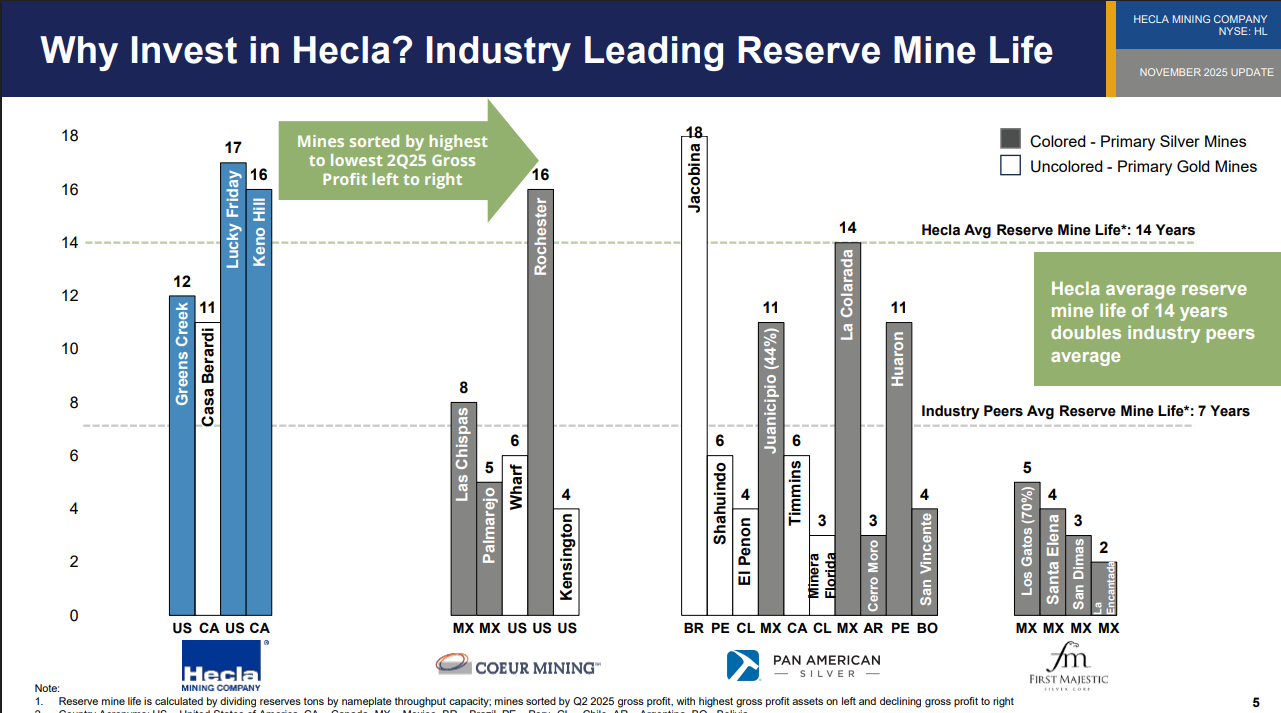

Silver reserves: 240 Moz P&P | the second-highest in the company’s history.

Silver production: 16.2 Moz | also the second-highest ever, driven by Greens Creek, Lucky Friday, and the ramp-up at Keno Hill.

Layer 2025 on top - a year where silver is up roughly ~70-80% YTD and gold has broken into its own structural leg higher - and HL has done exactly what a liquid sector bellwether should do: it’s rerated, it’s outperformed, and it’s now back on every generalist’s screen.

That’s precisely why it’s the right starting point:

If you want to understand how the market values silver producers at scale, you need to understand HL.

And if you mostly live in juniors, HL is the reminder of what “success” actually looks like; multi-asset, long reserve lives, strong FCF, low net leverage, heavy institutional ownership, and a premium that comes with being the benchmark.

This isn’t my kind of trade at today’s valuation.

But it is absolutely the right company to open this series with.

Business Snapshot

Think of this section as: What am I actually buying here?

Hecla in one line

A multi-asset, North American precious-metals producer with a heavy silver bias, operating four mines:

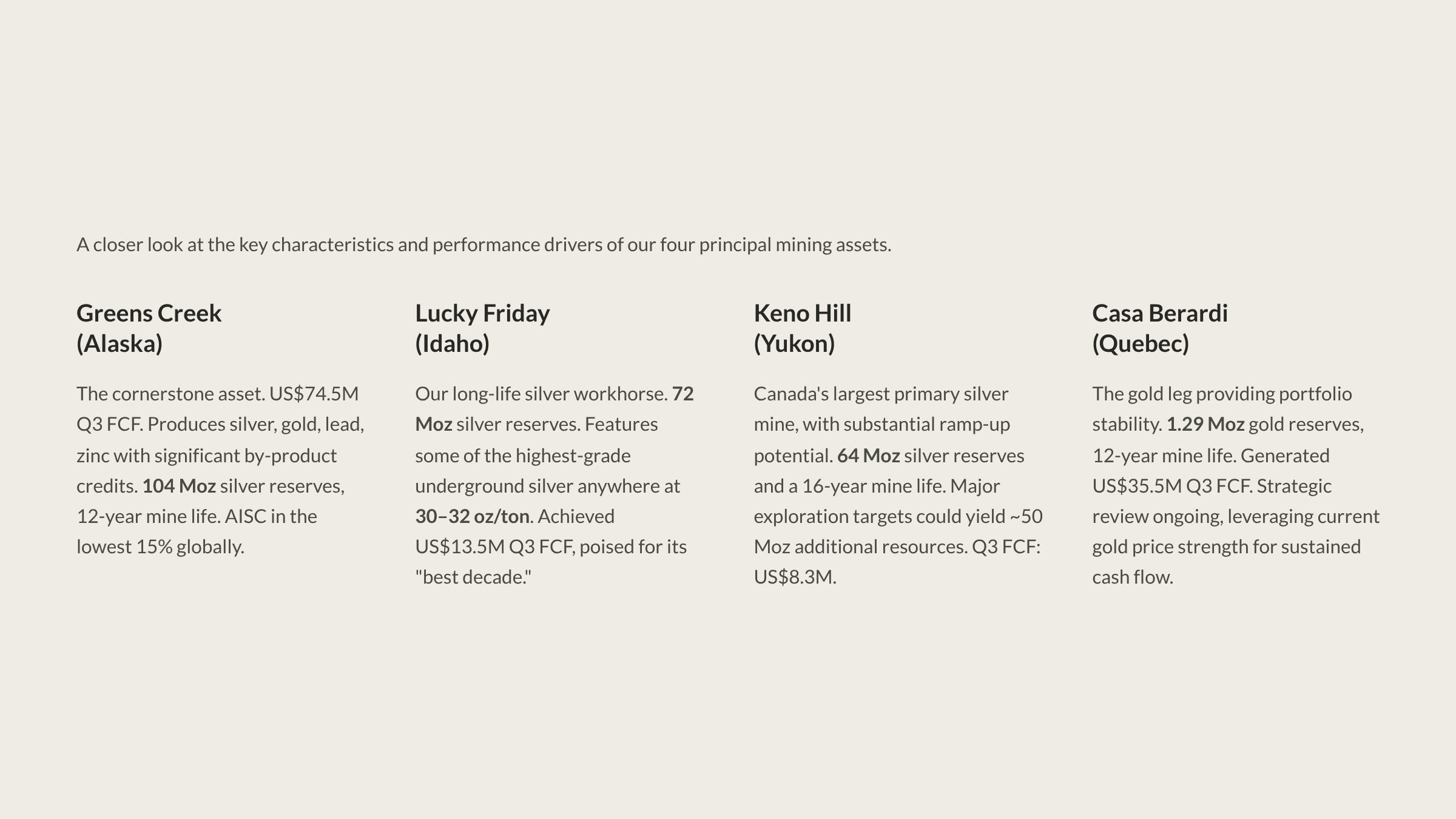

Greens Creek (Alaska): the cornerstone polymetallic underground mine.

Lucky Friday (Idaho): long-life, high-grade underground silver.

Keno Hill (Yukon): Canada’s largest primary silver mine, ramping hard.

Casa Berardi (Quebec): gold-dominant; good FCF at today’s gold tape.

Scale, listing, liquidity

Ticker: HL (NYSE)

Share price: mid-teens (recently around US$14–15, with a 52-week high at US$16.10).

Market cap: roughly US$9.5–10B at current levels.

Liquidity: tens of millions of shares trading per session; heavy institutional + ETF ownership (State Street alone holds >34M shares).

In other words: this isn’t a flyer. This is one of the global silver benchmark vehicles.

Production & Reserves

From the official 2024 reserve update:

Proven & probable silver: 240 Moz (second-highest ever).

2024 silver production: 16.2 Moz (also second-highest).

Gold reserves: ~2.2 Moz.

By-product exposure: meaningful lead/zinc credits at Greens Creek and Keno.

The most important insight:

Hecla fully replaces most of what it mines.

Reserve life doesn’t collapse on you if silver goes into a multi-year bull market.

Q3 2025 Financials | the cash engine

Valuation | premium quality, premium multiple

Here’s where HL becomes interesting:

Trailing P/E: 47–48×

Forward P/E: ~18–20×

Price-to-FCF: ~52× → ~2% trailing FCF yield

In plain English:

HL is not a value stock at $14–16.

It’s priced as a benchmark, not a bargain.

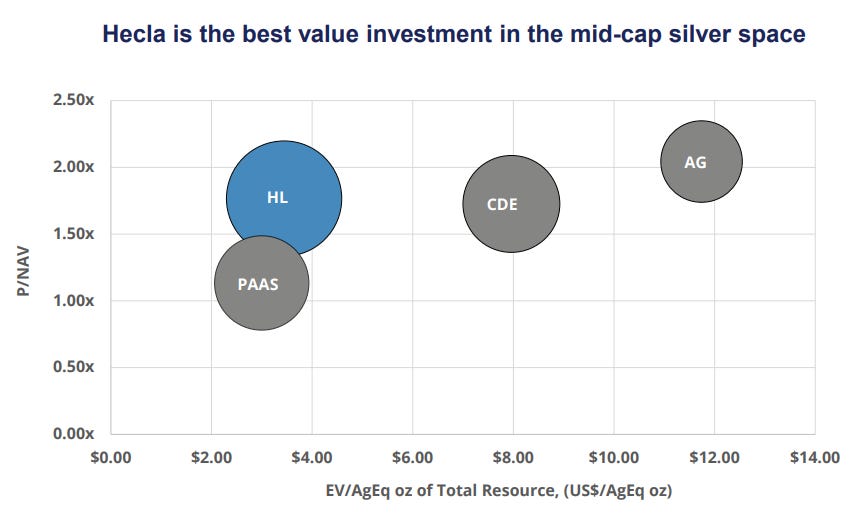

The NAV chart in the November deck (link) shows HL trading at a modest premium to the peer group; not absurdly stretched, but absolutely reflecting its jurisdictional profile, reserve life, liquidity and institutional ownership.

Is there a better value name in the same neighbourhood?

Short answer: Yes; Fortuna (FSM) still screens as the cleaner value vs HL.

FSM market cap: US$2.5–3.0B

Trailing P/E: 11–13×

EV/EBITDA: mid-single digits (well below HL’s high-teens)

That doesn’t make HL uninteresting; but it does mean you need a strong view on structural silver and quality premiums to justify paying the top end of the range.

The Asset Base | Four Pillars Across Tier-1 North America

Hecla’s November deck reduces the entire pitch into five bullets:

silver legacy, best jurisdictions, silver focus, reserve dominance, cost excellence.

The portfolio makes that real. All four operating mines are in Alaska, Idaho, Quebec and the Yukon, and the exploration optionality sits across Nevada, Montana and Colorado.

The Cash Engine | Margins, Mix, FCF, Balance Sheet

Let’s strip the Q3 numbers down to the operational truth.

Revenue mix | important nuance

In Q3 2025:

Silver: 47–48% of total revenue (up from low-40s in Q2)

Gold: ~37%

Lead: ~6%

Zinc: ~10%

So despite Casa Berardi, this is still fundamentally a silver producer, and increasingly so as Keno Hill and Lucky Friday contribute more ounces at higher prices.

Mine-level free cash flow | rare clarity

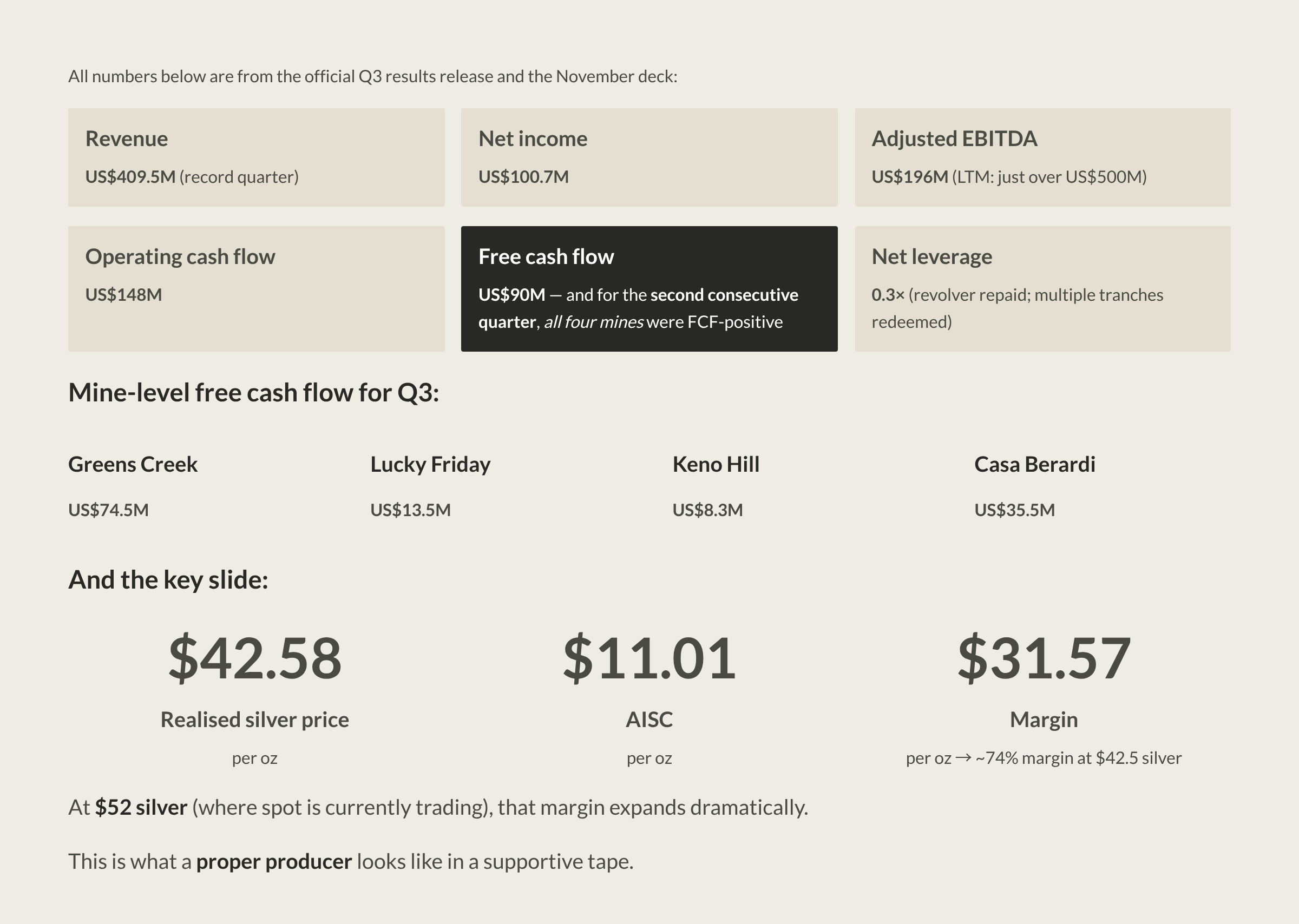

This is straight from the November deck:

Greens Creek: US$74.5M

Lucky Friday: US$13.5M

Keno Hill: US$8.3M

Casa Berardi: US$35.5M

Consolidated FCF: US$90.1M in Q3.

You almost never get a quarter where every single mine is FCF-positive.

HL delivered exactly that.

Margins and cost structure

Again, from the deck:

Realised silver price: US$42.58/oz

AISC: US$11.01/oz

Margin: US$31.57/oz → ~74% margin at the consolidated level.

At $52 silver, the incremental margin is enormous; the cost base barely moves, and almost all the upside drops to FCF.

Not many silver producers can say that today.

Balance sheet | risk no longer on the table

Adjusted EBITDA (LTM): ~US$506M

Net leverage: 0.3×

Revolver: fully repaid

Multiple debt tranches: redeemed over last ~24 months

This is not a balance-sheet story anymore.

This is a cash-flow story with a premium multiple attached to it.

Execution & Pipeline | Why HL Has Duration

The market often treats HL as “four mines and done.”

That’s not actually true.

There are three real optionality buckets baked into 2025–26:

(A) Exploration at existing mines | reserve life is not static

Greens Creek: US$9M 2025 exploration budget focused on extending Gallagher and other ore zones down-plunge and laterally.

Keno Hill: US$8.4M exploration budget, with aggressive drilling at Bermingham and Flame & Moth. Potential for ~50 Moz additional resources if current hits continue.

This is why HL’s reserve life stays elevated through multiple cycles: they don’t sit back.

(B) Nevada | Midas + Aurora (hub-and-spoke)

Long-term silver–gold optionality, partially permitted, with real infrastructure.

Combined inferred resources across Nevada assets: around 300M silver-equivalent ounces (company figures).

Existing mill, tailings capacity, and multi-target district within a ~75–100 mile radius.

Aurora is in the U.S. FAST-41 permitting track, with an EA decision expected in Q4 2025.

Multiple targets (Sinter Offset, Pogo) showing visible gold + vein continuity.

This doesn’t matter for today’s FCF but it absolutely matters for HL’s duration.

(C) Montana | Rock Creek & Libby (copper–silver)

Large-scale, long-dated leverage.

Combined inferred resources:

Over 300 Moz silver,

Nearly 3B lbs copper,

according to company materials and prior technical summaries.

Potential mine lives: 20–30 years each, on company assumptions.

Major permitting milestone recently achieved: FONSI (Finding of No Significant Impact) allowing exploration activities to advance.

This is deep optionality; not priced into today’s FCF, not needed for today’s valuation, but absolutely part of why institutions treat HL as a “forever” name.

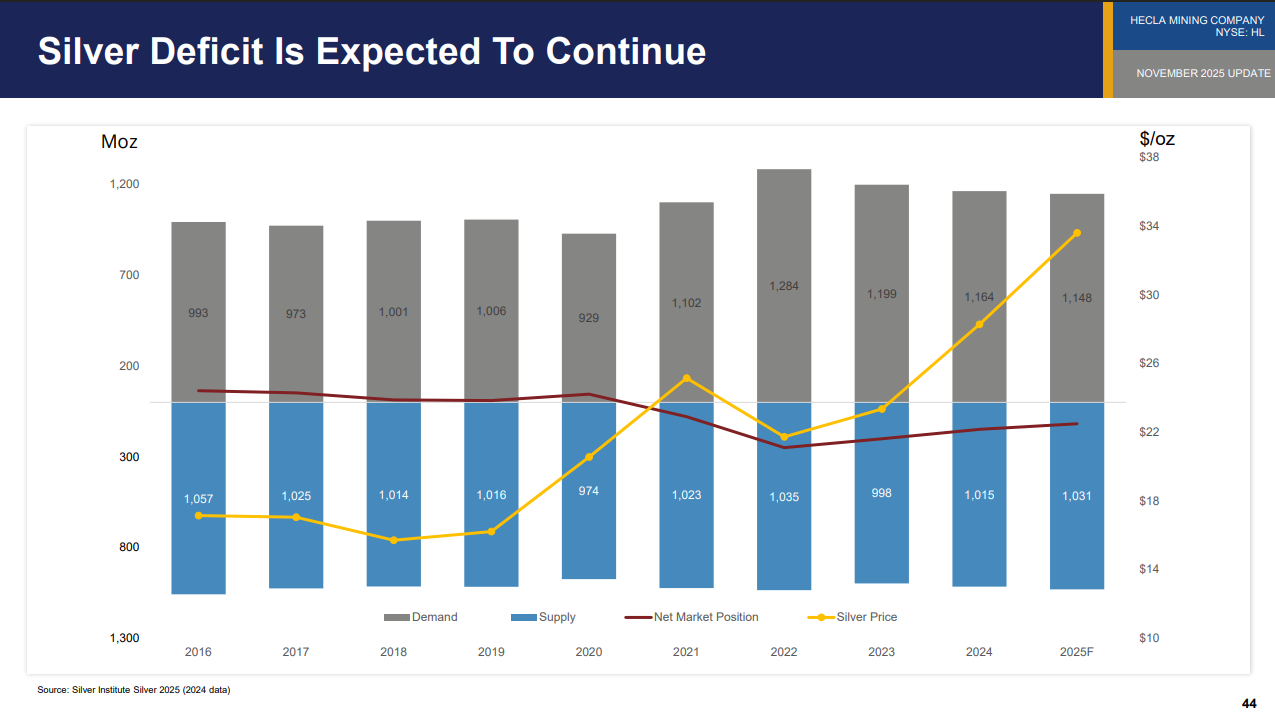

The Macro | Structural Tightness Isn’t Marketing

One of the cleanest slides in the November deck is the one titled essentially:

“Silver deficit expected to continue.”

It looks almost too simple - demand line above supply line - but that simplicity is exactly why the structural picture has legs:

Demand keeps compounding from multiple fronts:

Solar / PV: still the single biggest industrial driver.

Grid build-out: quietly pulling more silver into long-lived infrastructure.

Electronics, EVs: continuous, sticky base-load demand.

Investment flows: reawakened now that gold has decisively broken out.

Supply won’t magically fix itself:

Primary silver mines are rare.

Most silver production comes as a by-product from lead/zinc/gold mining.

New primary silver projects are barely trickling in; permitting, capex, financing, and ESG drag timelines out by years.

Grades continue trending lower globally.

If you believe in structural tightness - and I do, with the normal caveats on timing - then the next question becomes:

“What’s the cleanest expression of that view, depending on your risk appetite?”

For institutions, HL is one of the neat answers:

Tier-1 jurisdiction footprint

Long reserve lives

All four operations FCF-positive at spot

Low leverage, no balance-sheet drama

Pure scalability into higher silver prices

For more aggressive money, HL is not the answer but it’s the reference point everything else gets judged against.

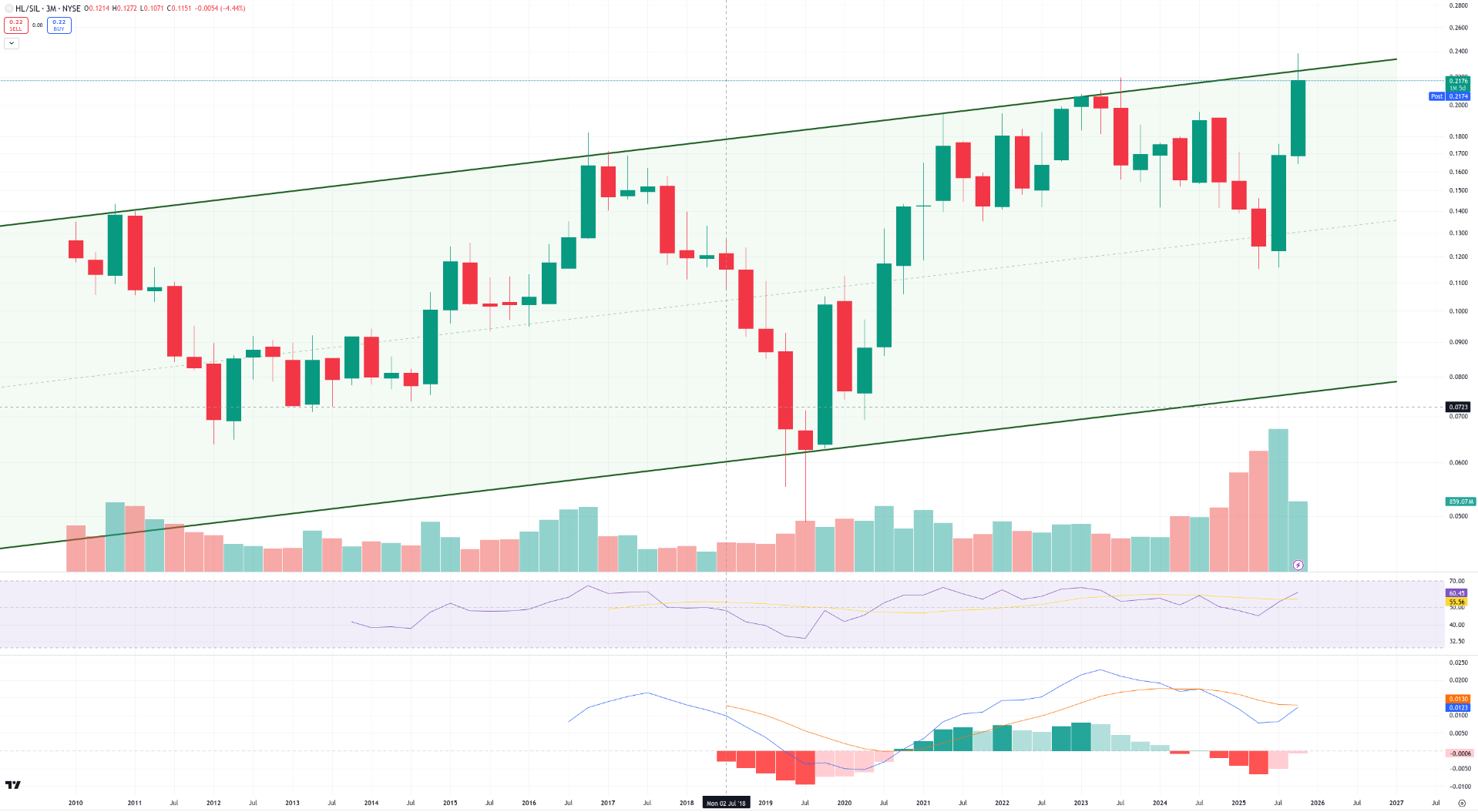

The Chart | What the Long-Term Structure Actually Shows

If you strip everything back and only look at structure, HL is doing what a sector leader should do in the early legs of a real cycle: it breaks out first, it trends first, and it stops caring about the noise that still affects the smaller names.

The first chart - HL/SIL - shows a clean, multi-year rising channel. That’s leadership behaviour. Every dip into the midline or lower rail has been bought, momentum resets cleanly, and the current quarterly candle is pushing back into the upper band with volume expanding. On a relative basis, HL is behaving like a stock that institutions have already decided is the default way to own silver beta without excess risk.

This is the entire point of having a bellwether: when the sector wakes up, the bellwether leads.

The second chart - HL/Silver - is the long-term lens, and it’s even more interesting. For decades, this ratio has lived inside a broad descending channel. Every cycle high in the ratio failed at the same upper boundary. Every downturn produced capitulation into the lower rail. But the current setup looks different: you’re getting a sustained rally right into that upper boundary with the largest volume the ratio has printed in more than 20 years. Momentum is turning, RSI has quietly broken its own downtrend, and the relative cycle lows now look like exhaustion rather than continuation.

You don’t need to overcomplicate what that means: HL is finally behaving like a stock that wants to exit a 30-year relative downtrend against silver itself. It hasn’t broken the structure yet, but the pressure is building from below, and in these long-term relative charts, that’s usually how trend changes start.

For me, the combination of the two charts is the signal:

Against miners, HL is already in confirmed leadership.

Against silver, HL is testing the final long-term ceiling with real momentum behind it.

That’s exactly what you want to see from the name that represents the institutional end of the sector.

Where This Fits in a Portfolio

The charts simply reinforce the way I already treat HL.

HL isn’t torque.

HL isn’t mispricing.

HL isn’t where you swing for 5–10x returns.

HL is the barometer.

It tells you whether the silver tape is healthy, whether flows are still supportive, and whether the larger money is accumulating exposure or stepping away. When smaller names get shaky, this is the chart I check first. If HL holds its structure - against SIL, against silver, and on its own weekly chart - then what you’re seeing elsewhere is rotation noise, not cycle failure.

And that’s exactly how I use it.

HL is a reference point:

strong enough to confirm the cycle,

liquid enough to show you where the real flows are going,

and stable enough that when HL stops working, you know the sector is actually changing character not just shaking out the usual suspects.

That’s the whole point of having a bellwether at the top of the watchlist hierarchy.