Junior Mining 101 | A quick primer for new readers

Every week in these updates I throw out terms like NPV, DFS, or EV/NPV discounts. If you’ve been around the sector for years, those words roll off the tongue. But not everyone starts with the same base layer of mining jargon. And if you can’t follow the process, it’s easy to miss why a stock can suddenly double, or why it gets cut in half after a single headline.

This note is a quick explainer. Think of it as your translation key. It won’t give you my proprietary workflow (that stays behind the curtain), but it will give you the tools to read these posts and know what matters.

Why juniors matter

Juniors are the farm team of the mining world. They don’t start with producing mines - they start with ground, ideas, and drill rigs. Their job is to turn geology into an asset that a major (or the market) values. The reason investors care: asymmetry. One success can offset a dozen failures, because the re-rating when a junior moves from “maybe” to “real” can be massive.

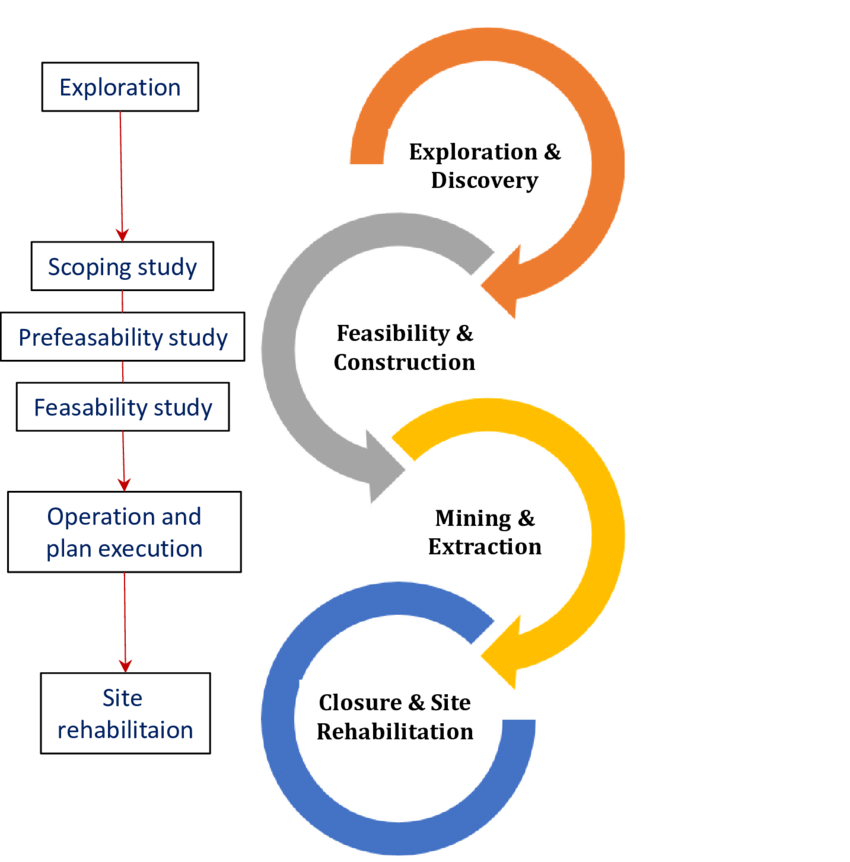

How the process usually unfolds

Exploration. Earliest stage: find anomalies, run geophysics, put in first drill holes. Sometimes you get the famous “discovery hole” - proof there’s real metal in the ground.

Resource. With enough drilling, the company publishes a Mineral Resource Estimate (MRE). Tonnes × grade. Categories matter:

Measured & Indicated (M&I) = higher confidence.

Inferred = lower confidence; needs more drilling.

A resource is not a mine. It’s the geological inventory.

Reserves. After engineering and economics are applied to M&I, part of it can become Proven & Probable Reserves. The mineable subset under realistic costs, recoveries, and mine design.

Economic studies. The acronyms:

PEA | Preliminary Economic Assessment. A first-pass economic snapshot (directional; ~±30–40% accuracy).

PFS | Pre-Feasibility Study. More engineering and tighter costs (~±20–25%); permitting typically starts here.

DFS/FS | (Definitive) Feasibility Study. The bankable blueprint (~±10–15%). This is what lenders/strategics underwrite.

From these studies come the numbers we track:

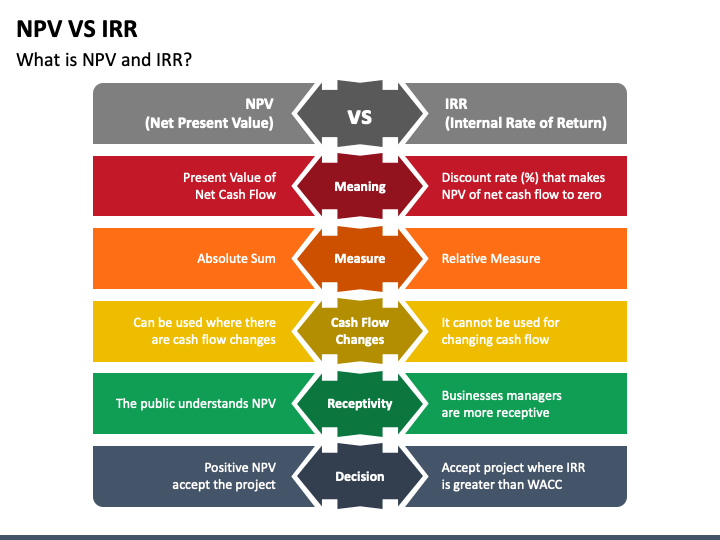

NPV (Net Present Value): today’s value of future cash flows. It depends on the price deck (assumed metal prices) and discount rate. Always check the sensitivity table.

IRR (Internal Rate of Return): the annualized return if built as planned.

Payback: how fast initial capex (build cost) is recovered.

AISC (All-in Sustaining Cost): “true” unit cost once sustaining capex is included.

Key levers: strip ratio (waste:ore), cut-off grade, recovery (what the plant actually captures), and for concentrates TCRC/payability/NSR (what smelters actually pay you for).

Permitting & financing. The valley of death. Juniors must secure permits, community agreements, offtakes, and a financing stack (project debt, royalties/streams, and some equity). This is where dilution risk shows up.

Construction & production. Once financed, it’s all about execution. Timelines slip, capex can creep. First ore/first pour is graduation day.

What moves the stock

It’s not just the process; it’s the milestones. Shares tend to react to:

Drill hits that expand size/grade.

Study upgrades (better NPV/IRR, faster payback).

Permits granted (risk down).

Binding offtake/financing (capex covered).

First production (execution proven).

Each step chips away at uncertainty, and the market prices that in.

How to read a study or news release in ~60 seconds

Scale & grade: mining method (open pit vs underground), throughput (t/d), headline grade.

Metallurgy: recoveries, concentrate specs/penalties, any pilot work.

Economics (post-tax): NPV/IRR/payback at the base price deck; scan the sensitivity tornado.

Costs: capex/opex realism vs peers; contingency and owner’s costs included?

Path to cash: remaining permits, funding mix, near-dated catalysts.

What can go wrong

This is a risky game. Key risks:

Commodity prices: juniors are price takers; if gold/copper falls, economics change overnight.

Permitting/community: delays or pushback kill timelines.

Capex creep: inflation, logistics, scope changes.

Dilution: serial raises at lows erode upside.

Metallurgy: if the rock doesn’t yield the metal, the model breaks.

That’s why I keep hammering on insider ownership, EV/NPV discounts, and balance-sheet strength. They’re your safety margins. (Quick note: EV = enterprise value = market cap + debt − cash. EV/NPV tells you how many cents you’re paying today for a dollar of project value under the study assumptions.)

Bottom line

If you’re new here, this is your crash course. From exploration through DFS, from NPV to EV/NPV, this is the framework behind every update. When I say “this trades at ~0.2× NPV with a DFS in hand,” you now know why that matters.

None of this is investment advice. Do your own work and size for volatility - juniors swing.

I feel like your x posts might actually make sense now 😂

Big brain content here Vinny.