Vanadium: The Rules Metal Nobody’s Watching (Yet)

This past week was a wild one; plenty of volatility, sharp reversals, and a few extremes across the Core 15.

Despite the noise, the portfolio finished up another 10 points, roughly +80 % in two months. That’s a great run, but it doesn’t mean the next two months will repeat it. Markets move in waves, not straight lines; our edge is staying early, selective, and grounded in fundamentals.

As per the poll I posted about ten days ago, this week’s deep dive goes to Vanadium: a sector that’s been asleep on the screen but quietly setting up a technical and structural base that’s hard to ignore.

Some metals move because of hype. Vanadium moves because of rules. When regulators raise the bar on steel strength, mills don’t get a choice, they reach for micro-alloying, and vanadium is first in line. Add the pull from large-scale vanadium redox flow batteries (VRFBs), and you get a small, opaque market that can flip from dull to explosive fast.

Prices are stuck in neutral. That’s what makes it interesting.

What makes vanadium stand out

Roughly 90% of vanadium goes into steel — mainly rebar and high-strength low-alloy (HSLA) steels. When China’s higher-strength rebar standard (GB 1499.2-2024) became mandatory on Sept 25, 2024, it effectively hard-wired vanadium demand into the building code. This is policy-driven, not cyclical: mills don’t get a choice — they have to use more vanadium-nitrogen alloy.

At the same time, vanadium redox flow batteries (VRFBs) are quietly tightening the market from the other end. The world’s largest installation - 175 MW / 700 MWh at Rongke Power - went live in 2024, and every gigawatt-hour of storage locks up physical vanadium for decades. Combine that with a thin, non-futures-based pricing structure - V₂O₅ $/lb (Rotterdam) and FeV $/kg V (EU, CN, US) - and even small supply shocks can create sharp price moves.

Prices remain subdued: 2024 averages were about $5.45/lb V₂O₅ (China) and $12.84/lb FeV (U.S.), while 2025 prints hover around $5.1–$5.3/lb V₂O₅ (Rotterdam). In short, the market is still pricing boredom just as structural tailwinds - steel standards and energy-storage demand - tighten beneath the surface. That’s what early looks like.

Two of our Core 15 names provide direct exposure to this setup, more on that below in the paid section, which now deserves its own update.

How pricing actually works (quick guide)

V₂O₅ ($/lb): the oxide benchmark most contracts use (Europe or China).

FeV ($/kg V): the steel alloy marker.

Discovery happens via Fastmarkets/Argus assessments, not an exchange. So volatility is real when liquidity dries up.

Supply concentration (and why small restarts punch above their weight)

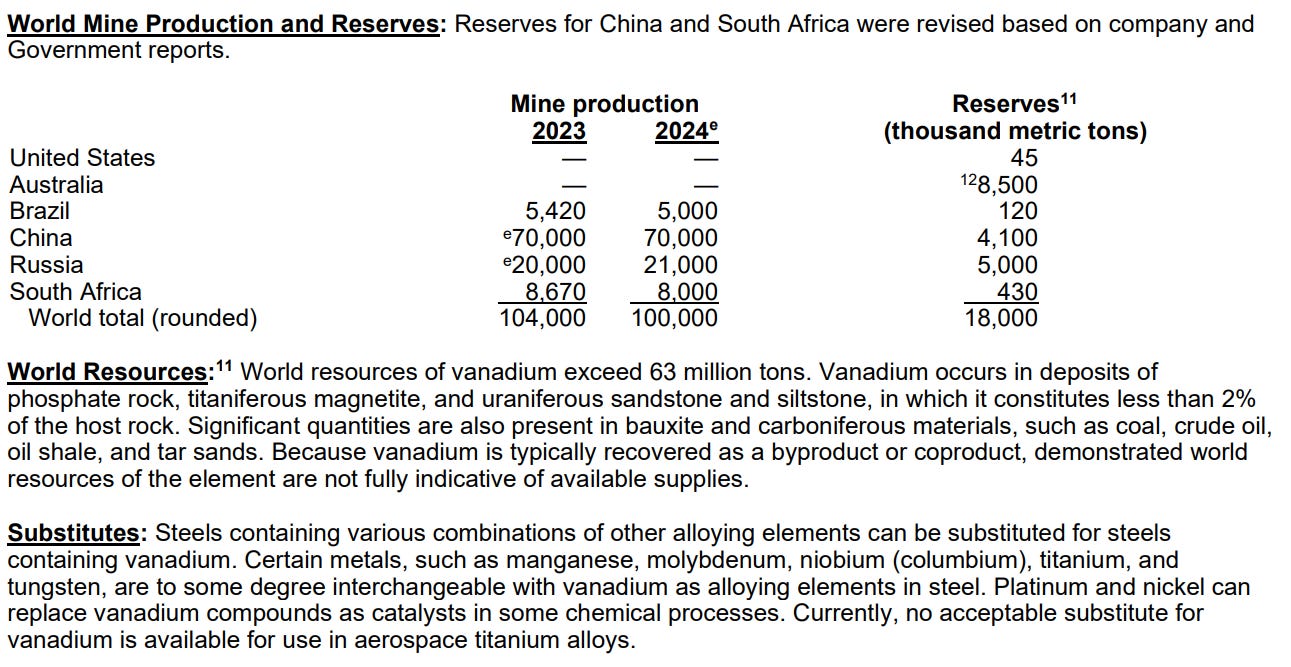

China still dominates production, with Russia and South Africa in the mix. Ex-China supply: Australia, the Americas, Europe - is creeping higher but remains small. Secondary supply from scrap and catalysts helps, yet data is thin.

That concentration is the risk and the opportunity: when one node stutters, V₂O₅ prices gap. The USGS 2025 sheet makes that clear - global tonnage is concentrated, and 2024’s price slide set up the current coiled base.

Source: USGS 2025 Vanadium PDF chart

2025 watchlist | three levers that can flip the tape

Rebar enforcement vs. property drag. The new Chinese rebar spec is the hinge. Real enforcement equals more VN alloy per tonne, which can offset slower construction starts. Early reports already hint at higher vanadium intensity.

VRFB commissioning cadence. Utility-scale flow batteries (like the 175 MW/700 MWh Rongke system) are live, with more multi-GWh projects lining up. Every commissioning cycle locks up more metal.

Ex-China execution. Even small restarts or financing wins outside China can move sentiment. With this kind of supply concentration, one new offtake can flip the tone from apathy to shortage overnight.

The chart view - why the setup looks asymmetric

Shout-out to new subscriber Spencer A for the sharp eye. He pointed out that the earlier vanadium chart I posted in this article over the weekend only ran through November 2024. I hadn’t noticed the x-axis cutoff at the time and had assumed the data was current.

For clarity, here are the updated charts using:

VAND.V (Largo Physical Vanadium Corp): which holds physical vanadium and serves as a decent proxy for the spot price.

LGO.TO (Largo Inc.): the primary vanadium producer, and a good industry bellwether.

VAND.V remains within a broad downward channel, while LGO.TO appears to be front-running the move, with a fake breakdown and re-entry into its long-term channel, a setup that often precedes trend reversal.

The bigger picture still holds: we’ve had nearly three years of compression since the 2022 highs, forming a long falling wedge that’s now coiling into a 2024–2025 base. Once that wedge resolves, the asymmetry becomes obvious - limited downside, sharp upside once momentum flips.

Add tightening steel standards and early VRFB demand into the mix, and the technicals finally rhyme with the fundamentals.

VAND.V (Largo Physical Vanadium Corp)

LGO.TO (Largo Inc.)

Investor playbook

Track the right prints. Stick to V₂O₅ (in-whs Rotterdam) and FeV benchmarks via Fastmarkets or Argus. Check weekly: don’t trade noise.

Watch enforcement, not headlines. The Sept 25 2024 Chinese rebar mandate compounds quietly. If mills confirm more VN in their blends, that’s your trigger.

Follow commissioning, not promises. Focus on operating VRFB megawatt-hours, not MOUs. The Dalian/Rongke system is the current anchor.

Size properly. Thin markets can whip. Build positions you can sit on through air pockets.

Know the catalyst ladder. Offtake news, restarts, tariff moves: that’s what wakes this metal up.

Bottom line

Vanadium isn’t a meme metal, it’s a rules metal. When the rulebook tightens, demand follows. Pair that with real flow-battery adoption and a thin, concentrated supply chain, and 2025–2026 could mark the turn. The market’s quiet now: that’s usually when it pays to listen.

We’ve been big on vanadium from the start.

Two of our Core 15 positions are pure-play vanadium names - that’s 20 % of the portfolio - so yes, we’re firmly positioned for this setup.

As always, if you want the entries, tickers, and catalyst trackers, you’ll find them in the paid section below, that’s where we keep the deep dives, updates, and valuation models.

In this week’s update you’ll also find:

Fresh news flow and context from the vanadium space,

A new weekly chart update, and

Minor rotations inside the overall Core 15 / Watchlist structure.

Stay tuned, and stay early.